Trading Signals & Macro Trends

Exclusive insights - Stay ahead of the market

1

US tariffs spark market risk-off mode; OPEC+ supply rise sinks Brent further

The US economy took a decisively protectionist turn last week, as President Donald Trump formally unveiled the long-anticipated tariffs – a sweeping set of import duties targeting virtually all US trading partners, with much stricter measures on selected countries with large trade imbalances. The announcement marks the boldest and riskiest US trade policy shift in decades and follows months of promises by the administration about eliminating trade deficits. Whether these tariffs are temporary negotiating measures to extract better deals from US trading partners or structural changes in the way the US approaches trade is hard to predict now, but it does look like it is going to be a combination of both. In particular, the universal tariff at 10% has many of the hallmarks of structural change, while the very high tariffs on individual countries appear to have elements of negotiating positioning.

Sign up to receive the full version in the future. (You will receive a selection of signals directly in your mailbox.)

2

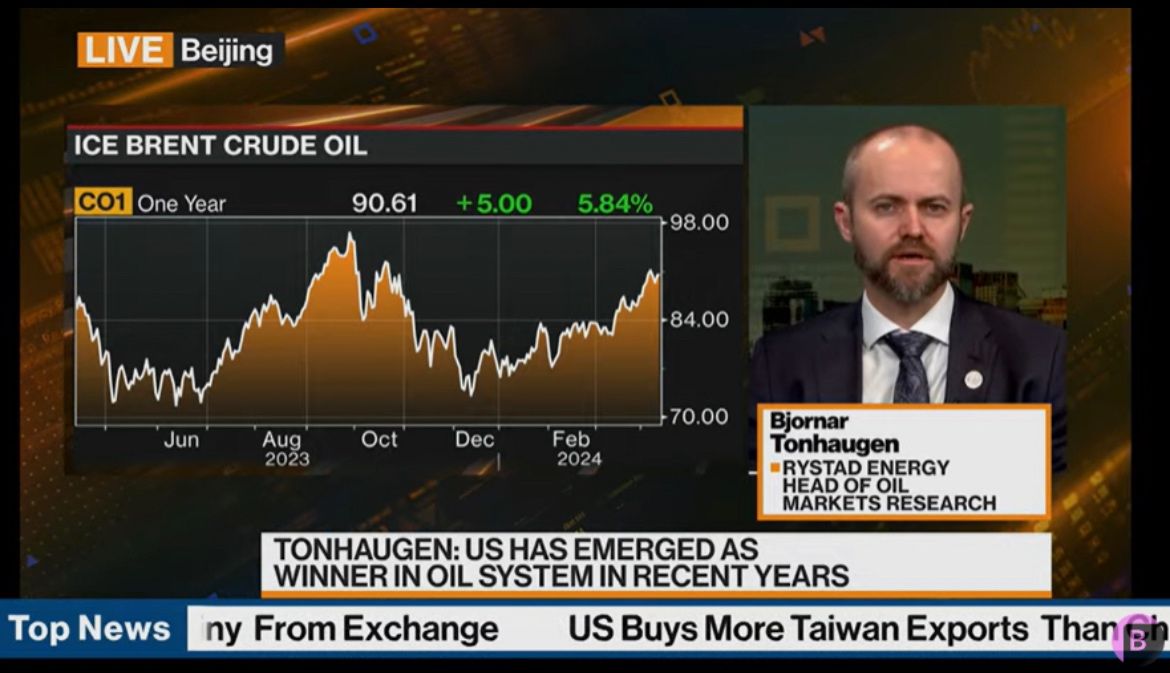

US oil production surges while imports slide

The US continues to lead global liquids production following strong year-on-year growth in March, driven by increasing output from the Permian Basin and the Gulf of Mexico. Rystad Energy estimates US oil production in March stood at 13.44 million barrels per day (bpd) of which 12.35 million bpd is crude oil and 1.38 million bpd is condensates. This is almost a 200,000 bpd uptick from 2024’s average output. Total liquids output in March came in at a staggering 22.89 million bpd with 7.08 million bpd of natural gas liquids (NGLs); an uptick of 800,000 bpd against the average 2024 liquids output of 22.43 million bpd. The significant jump is fueled by a mix of oil production growth in the Permian and the deepwater Gulf of Mexico (GoM) and a robust surge in NGL volumes from onshore wet gas plays.

Sign up to receive the full version in the future. (You will receive a selection of signals directly in your mailbox.)

3

OPEC+ May production boost contingent on US-driven supply disruptions

Highlights:

Brent has corrected by close to $5 per barrel and touched a level below $70 per barrel driven by the OPEC+ announcement to unwind cuts for May at three times higher than the anticipated 135,000 bpd. The expected demand surge from March to August provides the opportunity to test this unwind.

Rystad Energy estimates that the oil price slide below $70 per barrel will stay in check, driven by anticipation of summer demand and supply disruptions from sanctions and tariffs.

Along with this unwind, there is a strong message on compliance and staying within agreed quotas and limits to prevent any surplus and collapse of backwardation. OPEC+ actions are contingent on US tariffs, sanctions, or military-driven supply disruptions.

Sign up to receive the full version in the future. (You will receive a selection of signals directly in your mailbox.)

4

Russia update: Where would Russian barrels flow in peace deal scenario?

Key takeaways:

In short-term, we do not expect any effect in terms of production as Russia would follow OPEC+ plan and Russian producers would be able to increase production by 470,000 bpd by September 2026

We assess that a full ceasefire would immediately improve Russia’s refinery runs Base Case by around 150,000 bpd and would increase Russia's refined product exports by around 350,000 bpd, including around 250,000 bpd of diesel exports.

Lifting sanctions by US would decrease Urals FOB price discount from current $14-15 per barrel to $6-7 per barrel, ESPO from current $7-8 per barrel to $1-2 per barrel.

Sign up to receive the full version in the future. (You will receive a selection of signals directly in your mailbox.)

5

Agency comparison: Lower demand estimates, views remain fairly consistent

Key takeaways:

The latest round of oil market reports, including the US Energy Information Administration (EIA), the International Energy Agency (IEA) and OPEC, and our own updated Oil Market Balances Report (OMB) forecasts for March 2025, show that under the current OPEC+ policy, markets will face a serious surplus in supply for 4Q25 if OPEC+ implements unwinding of production cuts (excluding OPEC’s view). In this analysis, we compare their projections for 2025, providing key insights into the changing landscape of oil supply and demand.

Key takeaways from this month’s reports include:

Demand growth revisions: Demand growth estimates for 2025 have mainly been revised down by agencies. The downgrade is still within 100,000 barrels per day (bpd) in comparison to last month but it can accelerate in the coming months due to macroeconomic uncertainty. Only OPEC maintained its 2025 demand growth forecast at 1.45 million bpd, consistent with February’s estimate. Non-OECD countries are expected to be a key driver of growth as OECD demand growth has stalled. The IEA reduced its 2025 demand growth forecasts from 1.1 million to 1.03 million bpd amid the current trade war and global economic uncertainty climate. The EIA lowered its 2025 demand growth projection by 90,000 bpd to 1.27 million bpd due to an upward revision of demand level in 2024.

Call on OPEC+ crude: The IEA and Rystad Energy expect OPEC+ can increase production in 2Q25 and 3Q25 and still have balanced market. EIA projections implied that OPEC+ unwinding cuts will lead to surplus on the market from 2Q25. By 4Q25, the IEA, EIA and Rystad Energy have a consensus of a rather large surplus in the range from 800,000 to 1.6 million bpd. In the Base Case, the EIA expects flat production for OPEC+ for the rest of the year, which will keep Brent crude price in the range of $70 to $75 per barrel.

All agencies except for OPEC project liquids supply will surpass demand this year if OPEC+ increases production in line with the current plan. The glut is expected to be most significant in 4Q25, reaching 800,000 bpd for Rystad Energy and 1.6 million bpd for the EIA.

Sign up to receive the full version in the future. (You will receive a selection of signals directly in your mailbox.)

Crafted by experts